Buy These 5 ETFs To Replace Your Salary & Never Work Again

5 ETFs investors are using to pursue financial independence and early retirement.

How can you replace the income you earn from working for it with passive dividend income from the stock market by going over 5 ETFs you can consider investing in? No, it’s not a get-rich-quick scheme, and no, it’s not easy, but it 100% is possible if you’re willing to make sacrifices.

When most people think about investing their money, they think, “I want to go out and buy the stock for, let’s call it $100, and now I’m going to hope that it’s going to go up to $200. That way, I can make a lot of money.”

But there are 3 problems with these ETFs.

- Problem 1: The chance that the stock will not go up in value.

- Problem 2: Stock does go up to $200, well, you don’t actually make any money until you sell, and once you sell it, you no longer own this investment.

- Problem 3: You don’t know how long it’s going to be until you actually make any money, because it could take a day, a year, or a decade for the stock to go up in price.

And this is where dividends come into play, because some companies in the stock market have huge profits.

At the end of the year, they can do 3 things with these profits.

- They can save that money for an emergency.

- They can take that money and reinvest it back into the company, open more stores, hire more employees, and invest in more research and development.

- They can give that money away to their shareholders, people like me and you who own a piece of that stock. One way they can just give it away is through a cash payment called a dividend.

This money is literally deposited into your brokerage account, generally every 3 months, and you have to do nothing except own the stock.

Now, the nice thing about this dividend is that it doesn’t matter if the stock is going up or down; you still get paid your dividend. And you don’t have to sell your stock to get the dividend.

You get paid just for owning it. And you don’t have to wait. You get your dividend payment every quarter, meaning every 3 months, like clockwork. This money gets deposited into your account.

And this is where people get really excited. Now you go on to Google or ChatGPT, and you search for the highest dividend-paying stocks out there.

Now you find some amazing stocks paying out these huge dividends, and you think you’re going to get rich really fast, but that’s when you start to run into some problems.

The mistake that a lot of people make is that they think they’re investing for dividends for income. But that’s a big lie.

If you really want to have income, you should not be investing for income. You should be investing in a strong company that’s paying out income.

Because when you start to invest in companies that are paying out big dividends, what ends up happening is you have no idea what company it is that you’re investing in.

So, you buy this stock, you buy this fund because it has a huge dividend, and then what often happens is some months go by, and now the dividend starts to fall.

Why? Because the company itself wasn’t very good. And at the same time, the stock starts to go down.

So now, not only did you lose the income that you thought you were investing in, but you also lost the value of your investment because your company went bankrupt. So, it’s a lose-lose.

That’s why, if you’re going to be investing in dividends, you have to know how to find good dividend stocks or dividend funds to invest in.

Now, for this story, I’m going to be focusing on ETFs rather than individual stocks because ETFs tend to have less risk.

The difference between an individual stock, like McDonald’s, and an ETF is that when you invest in a company like McDonald’s, you’re investing in one company.

Now, yes, McDonald’s does pay a dividend, and I can invest my money into McDonald’s, but I’m taking on all the risk.

Because if McDonald’s does really well and they open up stores at every single street corner around the world, well, their stock is going to go up, their dividends are going to go up, and I am going to get rich.

But if McDonald’s doesn’t do so well, maybe they start producing some bad hamburgers, they start to get sued, well, now they could start to face some more struggles.

Maybe their stock price goes down, maybe the dividend goes down, but I’m taking on all the risk when I invest my money into McDonald’s.

Which is not a bad thing, but that’s going to require me to do more research on the company, keep up with the company, and study the financials in the company.

Versus the alternative, which is to invest in a fund. There are many funds out there that specialize in this type of dividend group, where now McDonald’s might be one of the stocks in this group, maybe Verizon is another stock in this group, maybe Apple is another stock in this group, along with dozens of other companies.

That way, now, if McDonald’s starts to do badly, this fund will kick McDonald’s out and replace it with another dividend-paying company.

That way, now, this fund is paying me dividends as opposed to me just relying on one stock.

That’s the advantage of using an ETFs as opposed to an individual stock.

But it also has its own risks as well because now, if I’m using an ETF and McDonald’s takes over the world, well, it’s going to be balanced out by some of the other losers in the fund.

So ETFs give you less risk, less upside, but if your goal is steady cash flow, where you don’t have to worry as much about the volatility, ETFs can help you do that.

And what I want to focus on today is ETFs that have shown strong growth of dividends over the last number of years, because ultimately, what you want to do is invest in funds that are going to be paying you more money year after year after year.

Can I guarantee that? No, absolutely not, because investing has risks. You are never guaranteed to make money when you invest.

In fact, you will lose money at some point. So, make sure you always do your own due diligence.

But let me go over some numbers, and then I’m going to go over specific ETF examples.

That way, you can potentially find a fund or an investment that can help you get to your income goals.

Let’s assume that your goal is to retire in 30 years and have at least as much passive income from dividends in the stock market to replace your job income, or maybe even more.

If you invest $1,000 a month for the next 30 years and you just put it into a savings account, and just for this example, I’m going to assume it’s growing by 0% a year, you’re going to retire with $360,000, and you are going to have 0 passive income.

But now, let’s say you become a little bit more financially educated and you decide to invest your money, but you invest your money like everybody else.

You invest your money for growth, not dividends, not income, and you get the average 401 (k) return, just about 8% a year.

Well, now you invest the same $1,000 a month for the next 30 years, you grow your money by 8%, and you are going to retire with about $1.5 million.

But remember, you have no income, which means for you to actually have money to spend, you have to start selling your investments.

But now, this is where things start to get really interesting. Let’s assume now that you’re investing the same $1,000 a month, you do this for the next 30 years, and you get the same 8% average growth of the stock.

So, we’re not talking anything crazy, but the stock is also paying out a 4% dividend. Again, nothing crazy.

Well, now what’s going to happen is you’re going to have the same $1.5 million as the value of your stock, but now you’re also going to be making some cash flow because you have a $1.5 million stock portfolio value that’s paying a 4% dividend.

Well, now that means you’re making $5,000 a month passively just from dividends from this dividend portfolio that you built.

Now, you might say, “Well, that’s not bad, but that’s not enough money for me to be able to retire.” Well, remember, you’ve also made about $450,000 in dividends over the last 30 years. I’m not counting that here.

But there’s one more example I want to describe to you. You were investing the same $1,000 a month for the same 30 years.

Your stock value is going to grow by the same 8% a year, so nothing crazy, and it’s paying the same 4% annual dividend. Nothing crazy. But the difference here is DRIP.

You are going to follow a dividend reinvestment plan, which means now every time you get a dividend, instead of taking that money and going out and buying a car, you’re going to take that money and reinvest it back into this fund.

That way, when you make money, you’re going to buy more shares of this dividend fund, which means it’s going to be buying you more cash flow every time you get paid.

And if you follow this dividend reinvestment for the next 30 years, meaning every time you get that cash flow, you just dump it back into buying more stock, well, now things start to look a little bit different.

Now your investment portfolio is not going to be worth $1.5 million. It’s going to be worth a little bit over $3.1 million.

And now you’re not going to be making $5,000 a month passively from dividends. You’re going to be making about $11,700 a month passively from dividends.

All because you stayed consistent with your dividend strategy. You invested in a strong company that was growing, not at crazy rates, but consistently.

And then the key is you reinvest your income for the next 30 years. That way, now you could have a solid stream of income.

And now that you understand the math, let me go over some specific examples to help you achieve these results, or maybe even potentially better.

Again, I cannot guarantee your returns, and past returns do not guarantee future returns.

But let’s go over some specific examples.

1. UNITED STATES COMPANIES

ETFs category number one, more on the safer side, is just to invest in the core foundational companies in the United States economy that are paying out strong dividends and have been working to grow those dividends. Let me go over a few examples.

Example 1: SCHD

You can buy it on pretty much any stock brokerage account.

This focuses on investing in high dividend-paying companies in the United States, but also companies that are working to grow their company, their profits, and their dividends year after year.

So, it’s focused more on those stable and growing companies.

SCHD is paying out a dividend of around 3.4% a year.

Over the last 10 years, they’ve grown their dividends by approximately 10.6% a year. This is their dividend growth rate on average over the last 10 years.

Example 2: An ETF called DGRO

This is an ETFcreated by iShares. This is focused on, again, dividend-growing companies.

But the difference between SCHD is that you only have to have grown your dividend for the last 5 years, as opposed to the last 10 years, like SCHD. So, it’s a little bit broader than SCHD.

DGRO is paying out a dividend of about 2.4% at the time of writing this story.

Over the last 10 years, they’ve grown their dividend by an average of 8.6% a year.

Example 3: VIG

(This is the Vanguard Dividend Appreciation ETFs).

This is a fund that’s investing in companies that have paid out and increased their dividend every year for at least the last 10 years.

So again, this one is focusing on a little bit more stability. It has a lower yield of about 1.5% dividend a year, but they’ve grown their dividend by an average of 7.7% a year for the last 10 years. The idea here is you’re getting less risk and higher quality.

E..xample 4: VYM

(This is another fund created by Vanguard.)

This is focused on the higher dividend-yielding companies in the United States.

This has a higher yield than VIG, which focuses on appreciation, but the appreciation growth every year is a little bit slower.

So, you’re getting about 2.3% dividends a year, and the dividends are growing by around 6.5% a year.

So now, you could put these numbers into a calculator to see if you’re investing your money consistently for the next 10, 20, 30, or 40 years, and your dividends are growing at rates like this, what does that mean for your income in the future?

2: INTERNATIONAL

Category number two is almost the opposite of category number one. Instead of focusing on the core United States stocks, now we’re going to go internationally.

Now, the nice thing about international companies and countries is that there’s more risk for more potential return.

Some of these countries have companies that are producing strong cash flows, so they’re paying out higher dividends.

So, let’s go over some international funds and what their dividend yields could look like.

Example 1: VYMI

(As a disclosure, I’m personally invested in VYMI.)

This is an ETF created by Vanguard that’s focused on high dividend-paying companies internationally outside of the United States.

Again, it comes with some more risk for potential return, but also some more diversification in your dividends.

This is currently paying out around a 3.5% dividend a year.

For the last eight or so years, because it hasn’t really fully hit that 10-year mark of data, it has grown its dividends by around 8% a year on average.

Example 2: SCHY

(This is a fund created by Schwab.)

This is another international ETF that focuses on high dividend-paying companies that are working to grow their dividends.

Now, the thing about this ETF is that it only started a few years ago, so there’s not a lot of data to back it just yet.

But right now, at the time, it is paying out around 2.3% a year and has grown its dividend by around 8.28% a year on average.

Now, let’s get slightly more aggressive on companies here in the United States focused on the mid-cap growers.

Mid-cap companies are those that are valued at $2 billion up to around $10 billion in value. So, they’re pretty big, they’re pretty established, but they’re not the Apples, the Nvidias, or the Teslas of the world.

Now, the nice thing about these mid-cap companies is they’re not the most risky companies out there, but they’re also at a stage where they can still grow. So, you can see even faster dividend growth with these companies.

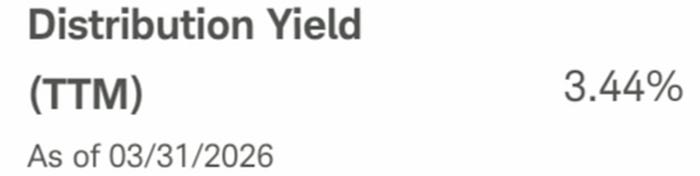

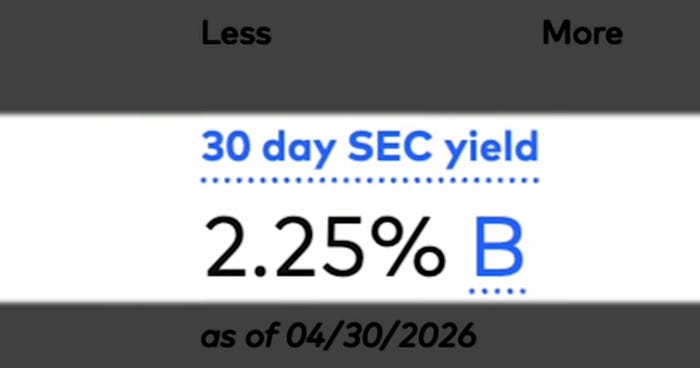

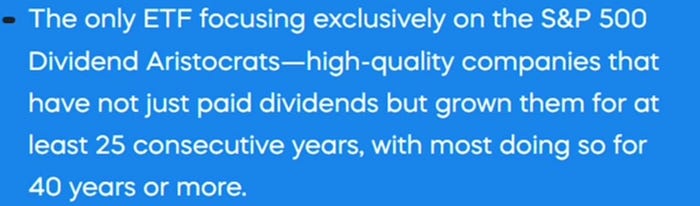

3. DIVIDEND ARISTOCRATS

We’re going to come back to the United States and remove some more risk. This is going to be one of the safer options, focusing only on dividend aristocrats.

A dividend aristocrat is a company that has worked to pay out and increase their dividend every year for the last 25 years.

The idea being, if a company has done this for the last two and a half decades, there’s a good probability they’ll do it again this year and next year.

Is it guaranteed? No, absolutely not. But the idea here is that it has a strong track record.

Example 1: NOBL

This is an ETF that focuses on S&P 500 companies, meaning they’re part of the 500 largest companies in the stock market, but they’re also dividend aristocrats.

So, companies that are part of the S&P 500 have also paid out and increased their dividend every year for at least the last 25 years.

At the time, it is paying out a dividend of around 2.3% a year.

Over the last 10 years, they’ve worked to pay out and increase their dividends by an average of 8.5% a year.

An alternative here is DGRW. This is an ETF created by WisdomTree.

This is focused on, again, United States quality dividend-growth companies, companies that have been working to pay out and increase dividends year after year.

At the time, it’s paying out a relatively low dividend of about 1.3% a year, but its dividends have been growing relatively quickly.

Over the last 10 or so years, it’s increased its dividend by about 13% a year on average.

4. MID-CAP COMPANIES

Now, for category four, we’re going to talk about mid-cap companies. These are interesting because they are not your Apples and Teslas of the world.

These are your companies that are valued somewhere between $2 billion and $10 billion. So, they’re also not your startups.

They’re already a pretty decent size, but they also have room to grow. So, there’s more upside potential with their dividends.

Example 1: REGL

This is an ETF that’s focused on dividend aristocrats that are part of the mid-cap stock range. So, these are companies that have been working to pay out and increase their dividends year after year after year. In this case, for over 15 years.

At the time of, REGL is paying out around 2.4% a year in dividends, but has been working to increase its dividends by approximately 11.6% a year over the last 10 years on average.

Then we have PEY.

This is an ETF created by Invesco that’s focused on not just companies that have paid out and increased their dividends every year, but also companies that have been working to increase their stock price.

At the time, it is paying out a dividend of around 4% a year with about an 8.1% dividend growth rate on average for the last 10 years.

And then, if you just want a little bit broader exposure to these mid-cap companies, maybe less of the companies that have paid out and increased dividends every year, less of those dividend aristocrats, you can take a look at something like DON.

This is an ETF created by WisdomTree. This is, again, giving you broader exposure to mid-cap companies.

At the time, it’s paying out around 3% a year in dividends, and its average annual dividend growth rate for the last decade is about 5.9%.

5. RISKY COVERED CALLS ETFs

The highest risk category, the one that I’m not the biggest fan of, but people have been seeing some success with it, and it’s been a growing trend, so I want to talk about it. This is focused on covered call ETFs.

This is more on the trading side of things. The idea is that it’s going to focus on certain trades where you don’t have to worry about the trade, but you’re investing in an ETF that’s focusing on finding trading opportunities that are going to pay you income through these dividends.

Again, more risk, more volatility, but more potential if that’s something that you’re interested in.

Now, without getting into all the technicals of how covered call ETFs work, the idea is you’re essentially buying a fund that’s renting out stocks to people that are trading these options, and in exchange, you’re getting this fee, this premium, and that’s what your dividend is.

So, it gives you more income today, but you don’t really see that compounding or growth of the income.

And then, when you’re in a bull market where markets are booming, there’s also a cap on how much money you’re making because then the options traders are also now exercising their options.

So, you generally just see more income today as opposed to more growth in income in the future.

Example 1: JEPI

This is a fund created by JPMorgan Chase Bank. This is again focused on these types of premium income stocks, where it holds S&P 500 companies and generates income by renting them out to options traders.

Over the last 12 months, it has generated about 8.2% in income.

Alternative number two is JEPQ.

This is again created by JPMorgan Chase Bank. It focuses on the same thing that I just talked about, but these are more focused on NASDAQ stocks as opposed to S&P 500 stocks.

At the time, over the last 12 months, it has paid out around 10.5% in income.

Now, the key for any of this to work is, number 1, to keep investing in your education. But also, number two, to keep consistently investing your money.

When it comes to things like dividends, you don’t just invest your money one time and then expect to be a millionaire by Christmas.

The way it works is you keep investing your money every month, month after month, year after year, decade after decade, to continually produce that income and then reinvest those profits.

It’s a strategy I call ABB, “Always Be Buying.” Buy when markets are up, buy when markets are down, buy when they’re sideways, and keep buying consistently.

And the only time you change your strategy is when markets go down. Use it as an opportunity to buy even more aggressively.

Because the mistake that a lot of people make is that they say, “I’m going to be a long-term investor. I want to invest in cash flow. I want to replace my paycheck with dividends.”

And then the next market crash happens, and now you sell out, now you lose all of your income, and you sell it for a loss, when that should be the time you’re buying even more because that allows you to buy more of these dividend-paying funds at a lower price, which allows you to increase your dividend income even faster.

If your goal is to replace your job income with dividend income, the way you do that is by consistently investing your money.

Because if you just put your money into a savings account, your money is not going to grow.

The average person is just trying to grow the value of their investments. But the problem with that is, there’s a chance investments don’t go up in value.

You have to sell your investment in order to get paid, and you don’t know how long it’s going to take.

You might end up waiting years or decades to see the returns that you want.

That’s where dividend investing can come into play. Dividend investing is where you’re going to invest in a company or a fund that’s going to pay you cash flow.

Generally, it’s going to pay money every 3 months into your account, and you don’t have to sell your investments, and you get paid while you wait.

Now, the nice thing about this type of dividend investing is that you can invest in individual companies, or you can invest in funds.

When you invest in a fund like an ETF, you have less risk because you don’t have to worry about managing your investment and making sure that the company invested in is still doing well.

You just want to invest in a strong fund. That way, you can keep continually investing in that fund.

And the thing that you want to pay attention to is not just how much income you’re getting, but how much income you’re going to get.

That’s why you want to pay attention to the strength of the fund itself, the strength of the companies inside.

One way that you can measure that is by taking a look at how much those dividends have grown over the past few years, because you want to see growth in the dividends.

That shows you that the profits are growing, which means not only are you going to make more income in the future, but the value of investments is going to go up as well.

So, we went through some numbers based on an 8% growth rate of the fund and how that can result in more income for you, assuming that you’re reinvesting your dividends.

Then we talked about how you can actually put it into action by talking about different categories of dividends.

- Category 1: Focused on core United States companies, and we talked about different types of funds that give you exposure to core companies here in the United States.

- Category 2: We went on the opposite side by focusing on international companies.

This is more risk, but more potential upside as well, because some of these countries are growing while the companies are also growing.

So, we talked about international funds that you could consider investing in.

Then we went back into the United States, but more focused on the aristocratic type of companies, companies that have been working to pay out and increase their dividends year after year after year.

The idea being that if a company has proven its track record for more than a decade, there’s a higher probability they will continue to increase its dividends in the future.

- Then, we started talking about mid-cap companies, the companies that are not the biggest ones in the world, but they’re already established.

So, they have the ability to potentially grow bigger in the future and pay out bigger dividends. So, we talked about some of those funds you can consider.

- Then we talked about the highest-risk category, which is the covered call ETFs. This has been growing in popularity, which is why I wanted to talk about it.

Again, the most risk, but you also don’t see that compounding growth in the value of dividends. It’s more of a short-term income play.

Again, if you got value out of this story, the best thank you was a referral. So, if you could please share this story with a friend, family member, colleague, or fellow investor, that way we can continue to spread this type of financial education. Thank you